Xtract One Technologies Inc. (XTRA:CA) q3’26 Earnings Update

Xtract One Technologies Hits an Inflection Point — Positive EBITDA, a $45mm Backlog, and a Security Market That's Just Getting Started

Xtract One Technologies is emerging as a leading provider of next-generation physical security solutions as a replacement for traditional metal detectors in critical environments with high foot traffic, including stadiums & arenas, hospitals, schools, office buildings, and industrial parks. The company has experienced a major inflection point in q3’26, turning to higher growth and profitability. With geopolitical tensions on the rise, Xtract One is quickly becoming a central theme to ensuring public security without hindering the convenience of mobility. With the increasing importance of public safety, Xtract One is positioned to continue its elevated growth path.

We initiated coverage of Xtract One Technologies in mid-February 2026.

All figures in CAD unless otherwise stated

Top-Line Performance

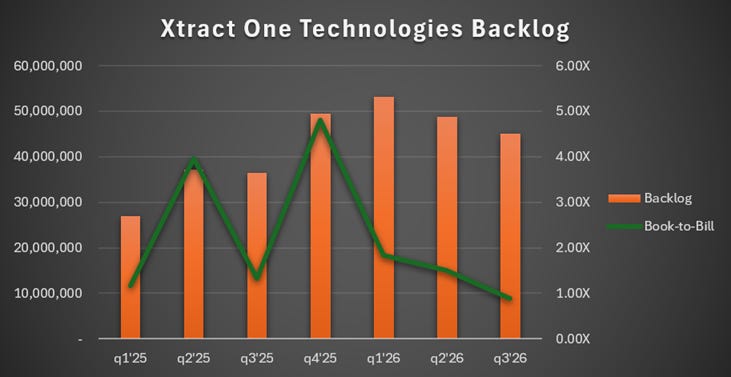

Xtract One delivered $10.3mm in net revenue in q3’26, equivalent to all of the first 3 quarters of FY25 for an annualized growth rate of nearly 200%, underpinned by demand for AI-enabled scanning technology. This equates to delivering Gateways to 16 distinct customers throughout the quarter. Xtract One closed the quarter with a backlog of $45mm and over $110mm in its qualified sales pipeline, providing a durable runway for growth that should compound revenue growth with the addition of the recurring services component of the product.

Xtract One added $9.1mm in new bookings in q3’26 for a book-to-bill ratio of 0.88x. 80% of the bookings in the quarter were subscription-based, meaning that these agreements will result in recurring revenue over time, smoothing out the revenue growth rate going forward. Adding to the subscription stream, the summer months tend to be higher product delivery periods given the transition from spring to fall semesters for schools, which may mean that Xtract One is set up for a strong runway of revenue growth for eFY27 given the growing deployments for its Gateways. Year-to-date, the booking split has been 60/40 upfront to subscription contracts based on seasonality of product deliveries.

To support the growing demand for the Xtract One Gateway and SmartGateway products, Xtract One has significantly expanded its manufacturing footprint to convert more backlog into revenue. Xtract One presently has 200 units pending delivery tied to upfront deals, valued at $27.2mm, the majority of which are expected to be deployed within the next 12 months.

Xtract One Technologies Operational Shift

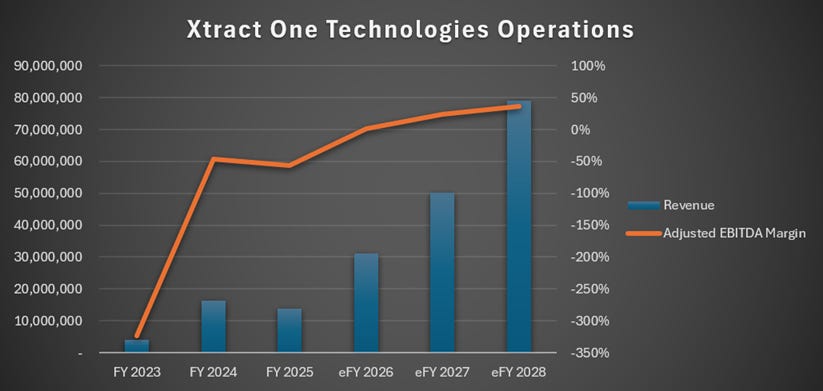

Xtract One delivered its first quarter of positive adjusted EBITDA driven by substantial improvements to operational leverage resulting from scaled growth. With larger volumes of sales flowing through the operating statement, particularly as Xtract One Gateway systems scale, margins should continue to improve as orders grow into the company’s operating footprint. Looking ahead, I’m forecasting this trend to continue, particularly as Xtract One delivers stronger recurring revenue with a higher product base, which should create scale with less incremental operating costs.

Xtract One Technologies Financial Forecast

Looking ahead, I’m forecasting Xtract One to maintain a stable, more durable runrate as it scales volume product sales, compounded by stability provided by annual recurring revenue from services growth. The combination of the land-and-expand model for product and software subscription services should drive profitability over the coming quarters, providing more certainty to growth rather than choppy periodic deployments. Given that Gateway deployments, in part, are out of Xtract One’s control given customers’ developmental timelines, an increase in subscription services on the larger Gateway base should smooth the revenue growth trajectory over time.

Xtract One closed q3’26 with $15.6mm in cash & equivalent and no debt on the balance sheet. Xtract One made some improvements to the balance sheet in the quarter, reducing its inventory on hand to 160 days, likely the result of the large ramp-up in product deployments in the quarter. Working capital may fluctuate from period to period depending on deployment timing rather than market dynamics.

Risks Related to Xtract One Technologies

Bull Case

Xtract One is scaling sales to operations, realizing significant improvements to operating leverage that has resulted in a turn to positive adjusted EBITDA. With a growing concern for security across offices, schools, hospitals, and other high-foot trafficked facilities, Xtract One may be in a position to continue its elevated growth trajectory over the coming years. A major catalyst will be the growing serviceable footprint with new product deployments, providing a broader runway for recurring subscription revenue that can further enhance margins over time. While the backlog contracted sequentially in q3’26, Xtract One has maintained a book-to-bill ratio of 1.30x year-to-date, suggesting a healthy flow of new bookings.

Bear Case

The market remains highly competitive and potential customers may elect to maintain their existing protocol, particularly if inflationary costs impact the total cost to operate. Xtract One is reinvesting in expanding its manufacturing capabilities and may not recognize the level of growth to sustain the larger footprint, potentially resulting in a return to negative adjusted EBITDA. Orders for Gateway products may be choppy from period to period and may not sustain the heightened level going forward.

Valuation & Shareholder Value

XTRA shares are currently trading at 6.28x price/sales, a relative discount when compared to the 1-year trading range. Despite the share price trajectory in recent months, I have reason to believe that XTRA shares can realize substantial growth going forward underpinned by improving operating performance and a higher growth market environment. With customer adoption quickly expanding, driving more depth in recurring subscription revenue, Xtract One should be in a position to maintain profitability and potentially exhibit more durability from quarter to quarter.

Given the upbeat performance in q3’26 and outlook for the market, I believe XTRA shares should be priced at $1.46/share at 7.29x eFY27 price/sales.

Using the model: the valuation table above references my financial forecast in the firm’s “financial position” section and ties it to the stock’s historical trading premiums. The trading premium array is derived through the normal operating cycle with the blue-sky scenario being the stock’s peak multiple and the gray-sky scenario being the lowest point. The target multiple aims for the midpoint, or the most likely trading range for the company’s stock. The trading multiples from there are set to a probability factor reflecting the likelihood of the stock trading at that premium given its historical trading range. From there, the trading multiple is tied to the probability factor to derive its relative market capitalization and relative multiple.

Disclaimer: No information found within this publication should be considered as investment advice. Information shares in this newsletter should ONLY be used for educational purposes. Monte Independent Investment Research and author are not liable for any financial decisions in relation to the information provided or discussed whether written or verbal. Information within this newsletter should not be shared or replicated. Information presented was independently written and is solely the opinion of the author.