Research & Analysis: Hubbell Inc. (NYSE: HUBB)

Hubbell Inc. Overview

Hubbell is in the business of developing and manufacturing electrical distribution infrastructure for the utilities sector as well as electrical solutions for industrial, non-residential customers. This market has turned to higher growth as the demand for electricity increases as a result of the reindustrialization of the US as well as the growing data center footprint.

Macroeconomic Impact

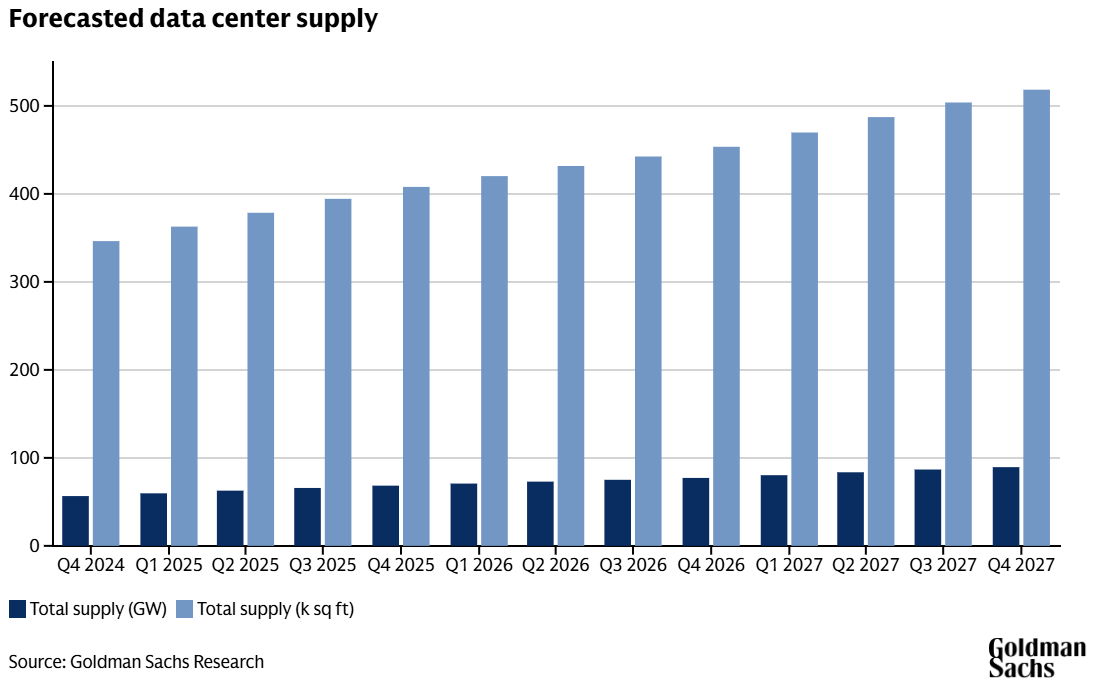

According to the IEA, electricity demand grew by 4.3% in 2024, an accelerated rate when compared to 2.5% in 2023. There are some estimates calling for an additional 128GW of power demand over the next 5 years, driven primarily by the growing data center footprint. The annual average load growth through the end of the decade is expected to be roughly 3% annually. Electric demand is forecast to increase by 15.8% by 2029.

For reference, the 8-building data center buildout in Texas as part of Project Stargate demands roughly 1.2GW of power.

Goldman Sachs estimates that power capacity across the global data center footprint will grow by 165% by 2030 to 122GW.

One of the biggest challenges faced by the hyperscalers is sourcing adequate power supply. Though not all data centers will command 1.2GW in capacity, there are several large-scale, 200MW, 400MW, and a handful of 1-2GW facilities that are being developed for hyperscaler and sovereign use.

An interesting phenomenon related to this matter is whether power will be supplied In Front of, or Behind the Meter. If the power station is built with the intent of being Behind the Meter, the load capacity acts as a dedicated power source for the data center. If the power source is In Front of the Meter, the facility will be a part of the grid, operated by a regulated utility, and may require additional infrastructure to manage and orchestrate load capacity between the data center customer and the grid.

As referenced in my report covering Constellation Energy (NASDAQ: CEG), FERC has been adamant in rejecting Behind the Meter access to the hyperscalers when partnering with regulated utilities. This factor was recently reiterated when FERC denied Talen & Amazon to have such an agreement in April 2025.

Despite this headwind, energy companies are working around this challenge. Chevron Corporation (NYSE: CVX) is entering into the market as a vertically integrated gas producer-to-power producer.

Overall, demand for utility & electrical equipment will likely fluctuate over time but remain in an upward trend through the end of the decade and beyond. In the near-term, gas capacity will be the primary solution for load capacity while nuclear is expected to begin adding capacity in the early-to-mid 2030s.

These two companies can act as leading indicators for the shift in power capacity as both engage in manufacturing gas turbines, nuclear infrastructure & small modular reactors [SMRs], and renewables.

Regardless of the power source, infrastructure will need to be built out to support the new capacity. In addition to this, grid modernization and hardening will also occur to support the additional capacity as well as ensure resiliency with the inclusion of intermittent sources like wind and solar.

We can at the very least make one broad assumption; electrical and utility equipment will need to scale to support new load capacity. With that, let’s take a look at this week’s single-name stock analysis, Hubbell Inc. (NYSE: HUBB).

Hubbell Inc. Operations

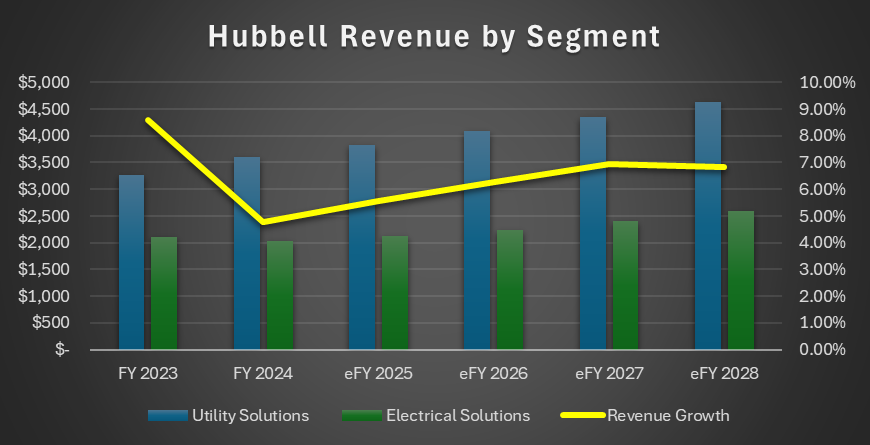

Hubbell reports under two segments:

Utility Solutions

Electrical Solutions

Utility Solutions

Hubbell primarily manufactures transmission & distribution components, substations, and telecommunications products in support of applications In Front of the Meter, meaning that these components are deployed by the utilities. Hubbell also develops a variety of infrastructure that serve the Edge of the utility infrastructure, including smart meters, communications systems, and control devices.

Markets supported in the Utility Solution segment include:

Electrical distribution

Electrical transmission

Water

Gas distribution

Telecommunications

Solar & wind

Electrical Solutions & Support

Hubbell’s Electrical Solutions segment covers infrastructure Behind the Meter, meaning that the components are utilized by building operators and industrial customers to manage energy throughput as well as critical infrastructure.

These components include critical electrical equipment found in facilities, including wiring device products, rough-in electrical products, and connector & grounding products.

The markets serviced by the Electrical Solutions segment include:

Light & heavy industrial

Non-residential

Wireless communications

Transportation

Data center

The vast majority of sales are in the US market, potentially exposing Hubbell to increased tariff exposure when compared to multinational firms. Accordingly, materials sourcing may create a significant headwind for Hubbell in the near-term until pricing action is fully implemented. Materials exposure includes:

China trade risks

Mexico/Canada [non-USMCA]

Steel & aluminum import duty

Increased material costs

Hubbell is largely exposed to a variety of commodities, which may impact margins over time. Major inputs include steel & aluminum, as well as other metals, as well as electronic components that may face pricing pressure following the recently imposed US import tariffs. Imported steel and aluminum are taxed at 50% as of June 4, 2025, a sharp increase from the previously announced 25% import tax. These tariffs include both the metals and their derivatives, potentially impacting future profitability for Hubbell. Where the current tariff policy stands, Hubbell is expecting to experience a $135mm impact to costs in eFY25. To counter these additional costs, management has engaged in price increases for product sales, potentially offsetting inflationary & tariff pressures to margins. Though not all product prices have been adjusted, management anticipates actions to be implemented throughout e2h25.

Keep reading with a 7-day free trial

Subscribe to Monte Independent Investment Research to keep reading this post and get 7 days of free access to the full post archives.